How Florida Small Businesses Can Avoid Payment Processing Fines and Fees

Most Florida small business owners are well aware of their processing rates. As they should be. Unfortunately, many issues with payments occur due to missing PCI requirements, confusion about pricing practices, debit card minimum violations, chargebacks, and hidden fees from processors. Accepting credit and debit cards requires much more than having an excellent rate. To […]

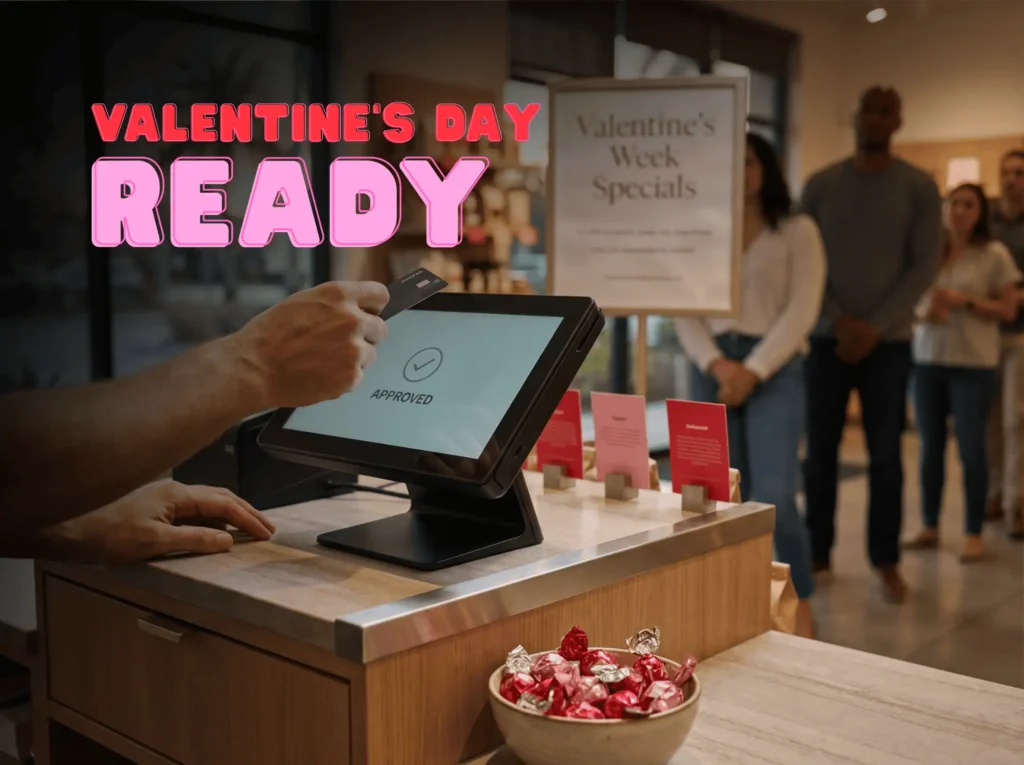

Avoid Lost Sales on Valentine’s Day

Valentine’s Day is far from just another day in Florida. It’s a full day rush. Lots of people show up last minute, wanting to get in, purchase something, and get out quickly. If there is a disruption in that flow they will probably walk away, and you’ll lose sales. According to NRF, Valentine’s Day spending […]

Slash Your Card Fees in 30 Days: Dual Pricing for Small Retail Shops

Credit card fees appear small when taken individually but they eat profit like termites. Two cents are stolen by one tap. Four more are taken by another swipe. By the time you close, the stack of lost pennies is large enough to hire a part-time employee. Dual pricing converts that hidden leak into found money […]

Gift Cards for Small Businesses: A Powerful Holiday Boost

Discover how gift cards for small businesses can boost holiday sales, attract new customers, and create free marketing opportunities. Perfect for seasonal raffles, gift baskets, and more!

7 Tips to Prevent Chargebacks from Hurting Your Business

Prevent chargebacks and protect your business with these 7 practical tips. Learn how to manage disputes, minimize losses, and maintain customer trust.

Do I pick a Local Merchant Service Provider or My Bank?

Choosing your Merchant Services Provider should be at the top of the list when opening a business Banks try to “simplify” the task for you by offering their in-house services. However, is the bank really better for your company than a Local Merchant Service Provider? The answer is no; the bank itself is just a […]